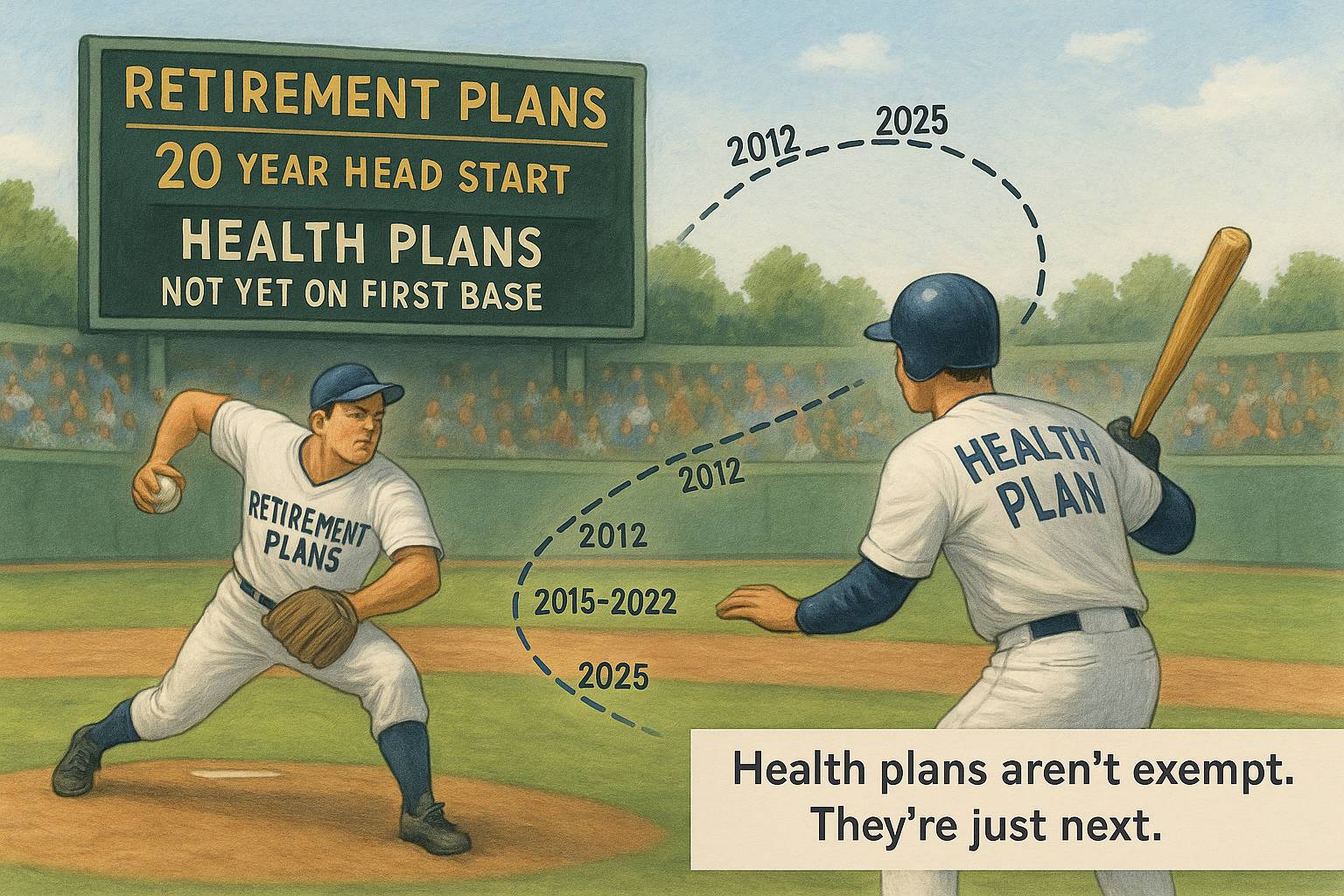

The fiduciary failures we fixed in retirement plans are repeating in healthcare—with higher stakes.

Retirement plan litigation forced a generation of fiduciaries to raise their game. They now operate with charters, processes, and accountability. Meanwhile, health plans—with far larger dollar flows—are still run with crossed fingers and handshake deals.

This issue explores the parallels—and shows how health plan fiduciaries can shortcut the learning curve by applying what 401(k) lawsuits already taught the benefits world.

Old Mistakes, New Consequences

You’ve heard the saying: “Those who don’t learn from history are doomed to repeat it.”

Well… health plan fiduciaries are living it.

Over two decades, retirement plan fiduciaries learned—sometimes the hard way—what ERISA really demands: loyalty, prudence, diligence. They built charters. Documented decisions. Kicked out conflicted vendors.

Health plan fiduciaries? Still flying casual and running out of runway.

Retirement Plan vs. Health Plan

ERISA Doesn’t Play Favorites

ERISA doesn’t care if it’s a 401(k) or a PPO—it still brings the same hammer. The same legal duties apply. The same liabilities apply. The same personal consequences apply.

But retirement plan fiduciaries have something health plan fiduciaries don’t: War stories. Paper trails. Legal scars.

Health plan fiduciaries are where retirement fiduciaries were 15 years ago:

Underestimating their legal duties

Over-relying on conflicted vendors

Overpaying for services

Operating with little documentation

Good faith won’t save you in court. Only a good process will.

If you wouldn’t run your 401(k) with limited oversight and hidden fees, why do it for your health plan?

Lessons from Retirement Plans

Chartered Committees Are the Standard Retirement plans use documented fiduciary structures. Health plans… not so much. Yet.

Vendor Compensation Must Be Transparent Retirement vendors disclose fees. Health plan vendors bury them—and most sponsors don’t ask.

Conflicts Get Scrutinized Plan brokers and services providers with financial conflicts are a lawsuit magnet. Sound familiar?

Process Trumps Performance Fiduciaries aren’t judged on picking the “best” option—but on using a documented, prudent process.

Plaintiffs’ Attorneys Have a Playbook And they’ve started turning the page from 401(k) plans… to your health plan.

Case Study: 401(k) Lawsuits Changed the Game

Tussey v. ABB Inc. The company’s retirement committee failed to monitor recordkeeping fees and allowed revenue-sharing arrangements that benefited the vendor more than the plan participants.

The result? A $36 million judgment.

But more importantly, it rewrote the rules:

No more blind faith in vendors

Shreddedthe “we didn’t know” defense

Document or get destroyed

Now apply that logic to your pharmacy benefit manager or third-party administrator.

Could you defend their compensation under oath… or would your lawyer suggest settling?

Don’t Reinvent—Repurpose

You already know how to manage fiduciary risk. You’ve done it for your 401(k). Now do it for your health plan.

✅ Create a fiduciary committee with a formal charter

✅ Request and review fee disclosures from all vendors

✅ Review and amend contracts for conflicts and gag clauses

✅ Adopt a Participant Interest Mindset™

✅ Ask: “Would a jury believe I acted in the best interest of employees?”

You already have the map. Stop thinking the road doesn’t exist.

Expert Perspective

Barbara Delaney helped steer retirement plans toward transparency. Her message to health plan fiduciaries? It’s time to catch up.

“Almost 20 years ago we turned our world upside down by providing a sound fiduciary process for our Plan Sponsors. The results, full transparency, fair and reasonable fees for services provided and better outcomes for all. I love a challenge, let’s go!”

Her call to action is clear: it’s time for health plan fiduciaries to adopt these proven practices.

The future doesn’t require invention—it requires application.

Key Takeaways

ERISA applies equally to health plans and retirement plans

Retirement fiduciaries raised their game after massive litigation

Health plan fiduciaries haven’t and it’s starting to show

The retirement side wrote the playbook—stop ignoring it

What happened to retirement plan fiduciaries years ago… is now coming for health plans.

Time to Reclaim Control

Your next headline shouldn’t be a lawsuit. It should be a success story.

Here’s what to do next:

🤝 Share this issue with someone responsible for a health plan

💸 SPECIAL OFFER: Newsletter subscribers receive 10% off any Validation Institute service. Use code FIDUCIARY10 at checkout.

validationinstitute.com

📬 PAY IT FORWARD: Feel free to forward this offer to your broker, PBM, or other vendors. Don’t hesitate to tell them you will favor validated vendors as part of your modernized procurement processes. Strong compliance and better benefits begin with validation.

Don’t be a bystander. Change the status quo and reap the benefits of The Health Plan Compliance Advantage.