The ERISA Trap 80% of Employers Have Already Triggered

Executive Brief

In a recent Health Rosetta webinar on the Schlichter Bogard lawsuits, ERISA attorney Julie Selesnick asked attendees to rate their confidence level on whether their voluntary benefit plans qualified for the ERISA safe harbor.

49% said they were confident.

Then she shared the data: more than 80% of voluntary benefit plans end up being subject to ERISA because they fail to meet the safe harbor requirements.

Half the room thought they were fine. Four out of five were wrong.

The Schlichter lawsuits just made this gap visible.

“I think many, many sponsors would be unpleasantly surprised to realize their voluntary benefits probably are subject to ERISA.”

Julie Selesnick, ERISA attorney

This issue breaks down why the safe harbor is stricter than most realize, what the lawsuits actually allege, and how to audit your own exposure.

ERISA Safe Harbor Gap

The Safe Harbor Is Stricter Than You Think

Most employers assume voluntary benefits fall outside ERISA. The plans are employee-paid. Participation is optional. The employer contributes nothing.

Feels like a safe harbor. No fiduciary duty. Nothing to worry about.

Except the safe harbor has four requirements, and most employers fail the third one.

The Four-Part Test:

The employer contributes nothing to the plan (including no pre-tax contributions or HSA/HRA reimbursement)

Participation is completely voluntary and clearly separate from core benefits

The employer has only a limited, non-endorsing role allowing payroll deductions and giving carriers access to employees, but nothing more

The employer receives no profit or benefit beyond reasonable administrative compensation

The third part is where it tends to fall apart.

According to a 1994 DOL advisory opinion still cited today, endorsement exists “if the employer urges or encourages any sort of participation or engages in any conduct that would reasonably lead members to conclude the program is part of an employer-established benefit arrangement and that includes expressing any positive or normative judgment about the program.”

If you host enrollment on your platform, you have facilitated it.

If you selected the vendor, you have administered it.

If you promote the benefit to employees, you have endorsed it.

Julie’s assessment: “This is a very difficult, strict safe harbor.”

The 5500 Problem

Every employer named in the Schlichter lawsuits included voluntary benefits on their Form 5500. This matters because only ERISA-governed plans require 5500 filings. By including voluntary benefits, these employers effectively conceded ERISA applies.

Julie called this “a killer at the motion to dismiss stage” meaning courts will likely allow these cases to proceed based on this evidence alone.

The problem: many employers include all welfare plans in a wrap document and report everything through a single 5500 filing. Often on the advice of their brokers.

If your voluntary benefits appear on your 5500, you may have already answered the ERISA question whether you intended to or not.

“I think we’re going to have to revisit it,” Julie said.

What the Lawsuits Actually Allege

The Schlichter Bogard complaints include household names.

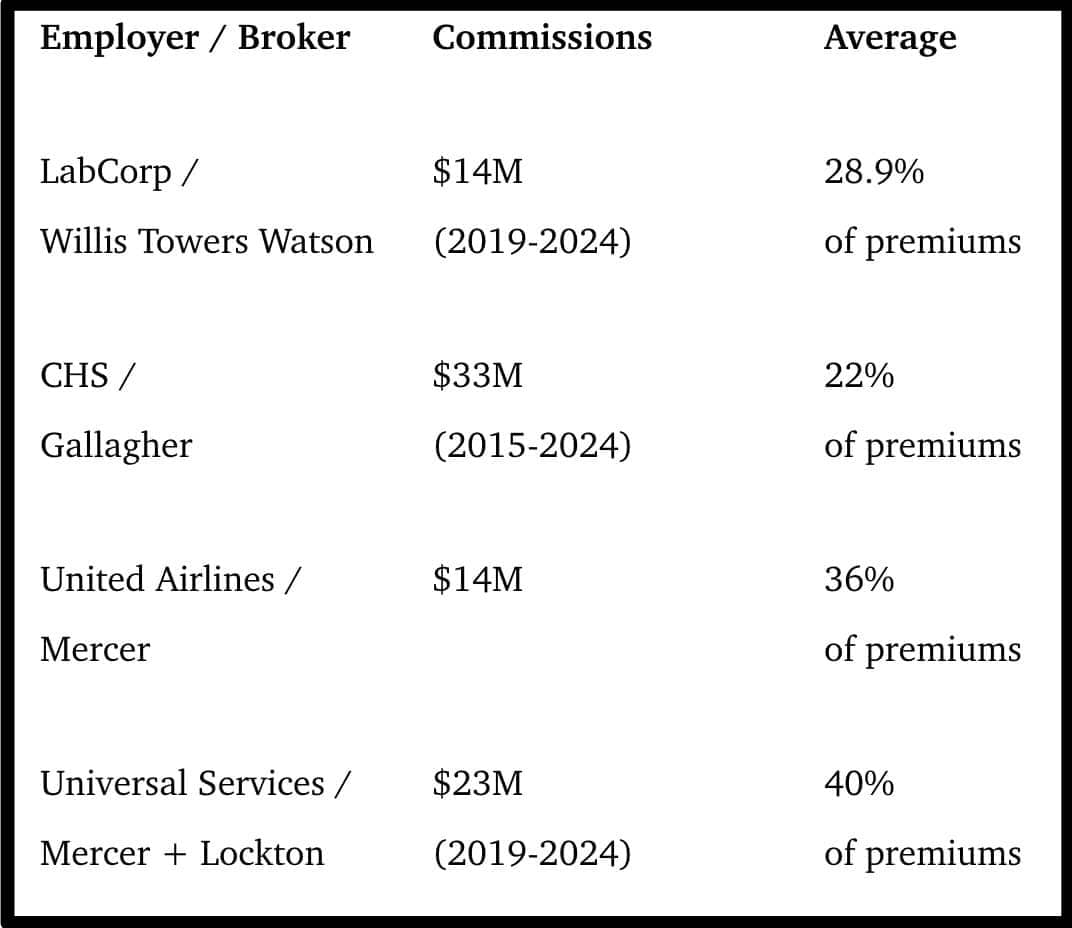

Employers: CHS/Community Health Systems, Universal Services of America, Laboratory Corp. of America, United Airlines

Employers failed to engage in any prudent process when selecting voluntary benefit products

Employers failed to monitor broker commissions or loss ratios

Brokers received commissions ranging from 22% to 40% of premiums

Industry benchmarks suggest 2% to 10% is typical

Loss ratios on these plans run as low as 18% to 23% (compared to 85% required for major medical under the ACA)

Julie’s summary: “These are real fiduciary process failure types of allegations.”

The complaints allege employers had no RFPs, no benchmarking, no vetting, no documentation. Even employers with strong fiduciary practices for health plans and 401(k)s applied none of that rigor to voluntary benefits.

The assumption was simple: voluntary means exempt.

The assumption was wrong.

The Commission Reality

Julie walked through the specific commission allegations:

Schlichter Voluntary Benefits Lawsuits

“In other plans, really less than 10% is the average,” Julie noted. “And 2% to 8% is more common. So 28% or 29% would definitely be way outside of that range. A real outlier.”

The complaints argue these embedded commissions are prohibited transactions under ERISA. And thanks to a recent Supreme Court case (Cunningham), prohibited transaction claims are now easier to survive past a motion to dismiss.

The question for every employer: do you know what your brokers earn on voluntary benefits? If the answer requires a phone call, you have a disclosure problem.

The Fiduciary Duty You Already Have

Here’s what changes once the safe harbor is lost: full ERISA fiduciary duties apply.

It no longer matters the employer pays nothing toward premiums. If the plan is subject to ERISA, the employer’s fiduciary obligations kick in. And if brokers are found to be fiduciaries, or even “knowing participants” in a fiduciary breach, they face liability too.

Julie emphasized the disclosure obligation falls primarily on employers: “The onus is on the employers. They’re not saying service providers have an obligation to disclose. They’re saying employers have an obligation to get this information because they’re the fiduciaries.”

You can’t know if you’re paying reasonable fees if you don’t know what you’re paying.

The Voluntary Benefits Fiduciary Playbook

If voluntary benefits are on your platform, here’s what fiduciary oversight requires:

Confirm your ERISA status. Get your committee together. Look at all voluntary plans. Determine whether each one meets the four-part safe harbor test or whether ERISA applies.

Audit the endorsement question. Review where voluntary benefits appear. Benefits guide? Enrollment platform? 5500 filing? Each touchpoint may constitute endorsement.

Identify the responsible fiduciary. Who oversees voluntary benefits? If the answer is unclear, start there. If someone is responsible, confirm they understand their fiduciary obligations.

Confirm board authorization. The responsible fiduciary should be formally appointed and acknowledge their role in writing.

Demand compensation disclosure. Request and review full documentation of all broker voluntary benefit compensation including commissions, bonuses, and overrides.

Benchmark against alternatives. Compare current offerings to market alternatives using documented criteria. If you have never run an RFP on voluntary benefits, you have a gap.

Evaluate loss ratios. Understand what percentage of premiums actually pays claims. If the answer is below 50%, your employees are funding a fee machine.

Establish a charter. Define objectives, governance, and oversight processes for voluntary benefits specifically.

Document everything. Create meeting minutes, selection rationale, and decision records. Courts ask for documentation.

What to Do First Thing Monday

Pull your Form 5500. Are voluntary benefits included? If yes, you may have already conceded ERISA applies. Put this on your fiduciary committee agenda.

Request broker compensation disclosure. Ask for full written documentation of all commissions on voluntary benefit products.

Audit the safe harbor test. Walk through all four requirements. If voluntary benefits appear in your benefits guide or enrollment platform, assume fiduciary obligations apply.

The fiduciary failures we fixed in retirement plans are repeating in healthcare with higher stakes.

In Closing

Julie shared another statistic worth considering:

75% of employees trust their employer to offer voluntary benefits that are good for them.

They trust you.

The Schlichter lawsuits exposed what happens when that trust operates without oversight. The employers and brokerages named operated the way most of the industry operates. The difference is they got sued first.

The safe harbor is stricter than most realize. The fiduciary duties are the same whether you’re overseeing a 401(k) or a health plan. The tools to get this right exist.

The Fiduciary Handbook, updated for the Schlichter Bogard lawsuits and available free through Nautilus, includes the Fast Start Kit with templates for everything courts will ask for: committee charters, acknowledgment letters, conflict disclosures, meeting minutes, and self-assessments.

Your employees trust you to get this right. Here’s how to deserve that trust.

All the best,

P.S. Julie put it plainly: “Even though you might get bored of hearing a bunch of us always saying how important the fiduciary process is, in a plan subject to ERISA, this becomes critical.”

Next week: what a fiduciary committee structure actually looks like in case courts come asking.

📤 Share: Forward this issue to your CEO, CFO, or General Counsel

💸 SPECIAL OFFER: Newsletter subscribers receive 10% off any Validation Institute service. Use code FIDUCIARY10 at checkout.

A Note of Appreciation

Julie Selesnick is the founder and principal attorney at Health Plan Leg

al Counsel PLLC. HPLC is focused on providing legal and consulting services to health plans, vendors to group health plans, and other stakeholders in the ERISA and non-Federal governmental employer sponsored and Taft Hartley health plan space.

Don’t be a bystander. Change the status quo and reap the benefits of The Health Plan Compliance Advantage. Schedule an introductory call with us.