How One Recommendation Led To A $105 Million Lesson

Executive Brief

Thirteen years is a long time to be a defendant.

In December 2006, John W. Cutler, Jr. was doing his job. As Director of Pension and Thrift Management at ABB, Inc., he staffed the Pension Review Committee and made recommendations about the company’s 401(k) plans.

One of those recommendations was to replace the Vanguard Wellington Fund with Fidelity Freedom Funds. That recommendation made him a defendant in a lawsuit that would span the next thirteen years of his professional life.

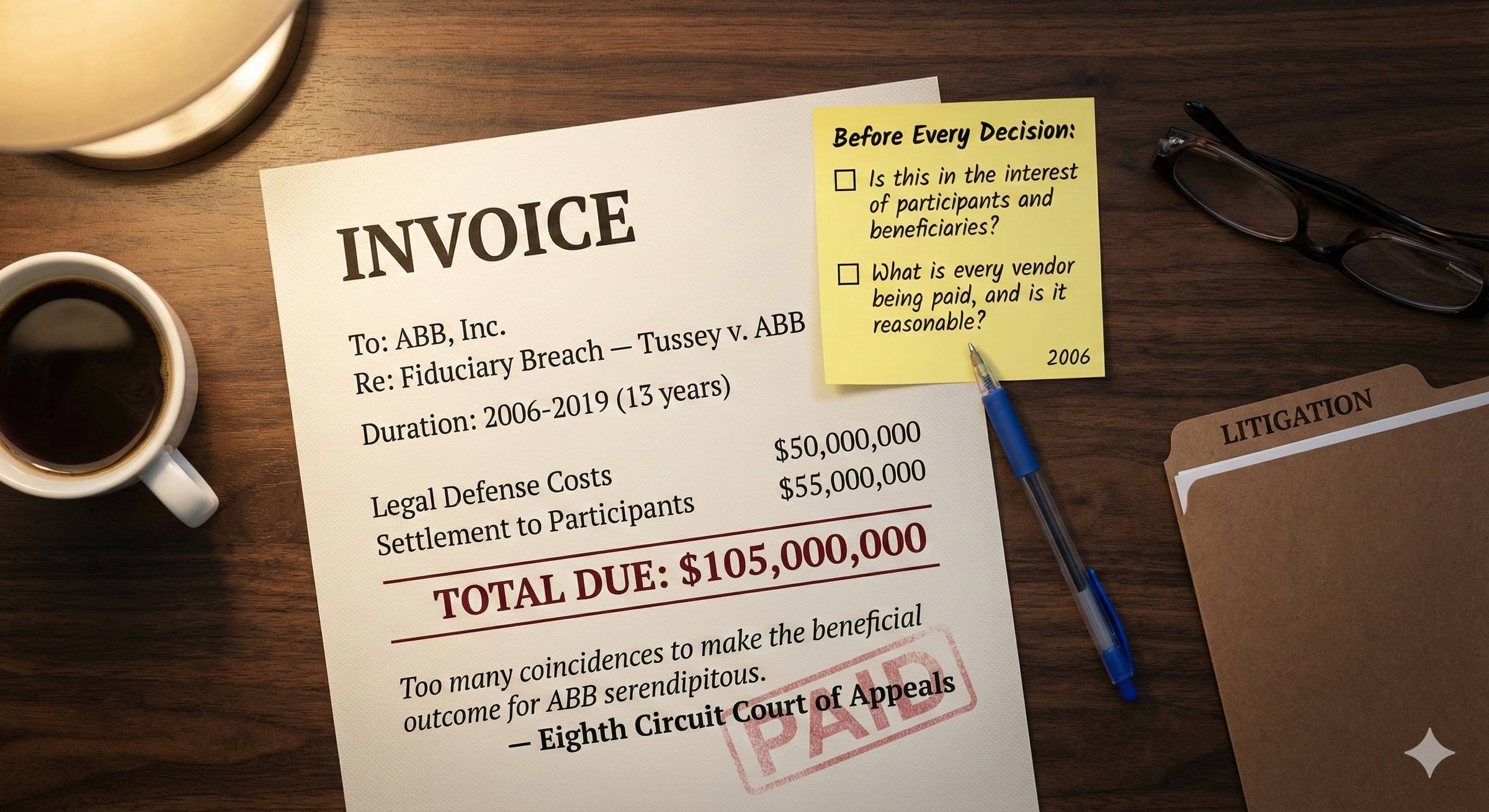

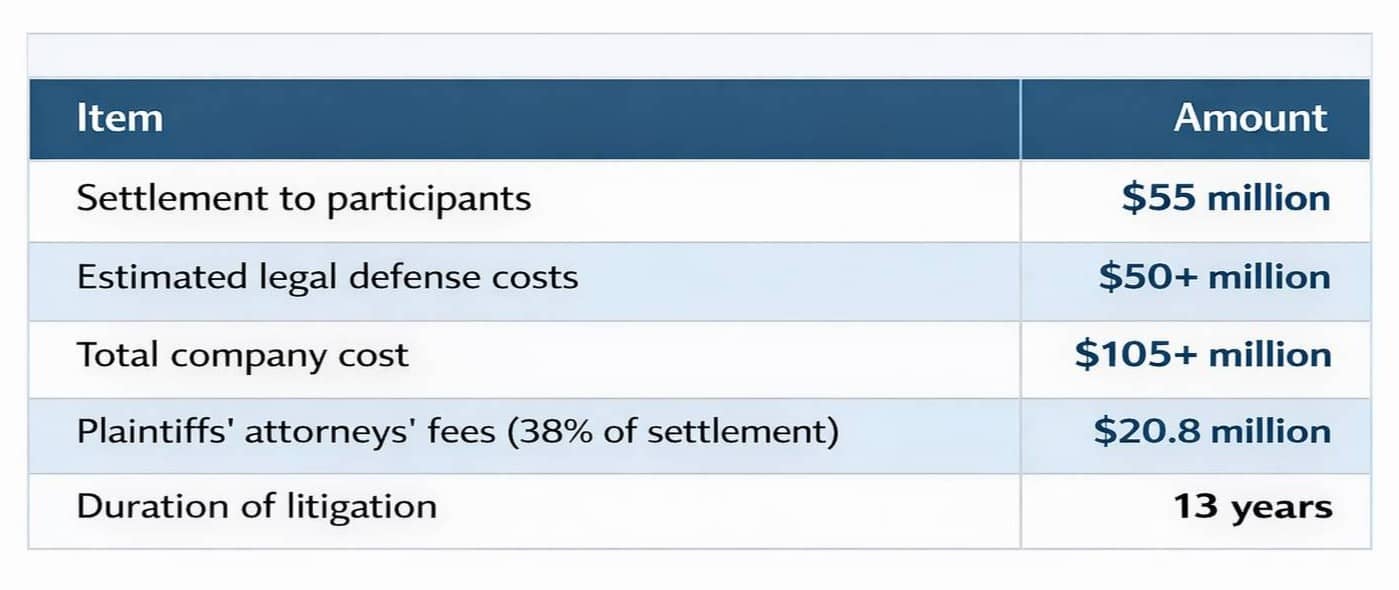

A four-week bench trial. Two appeals to the Eighth Circuit. Two petitions to the Supreme Court (both denied). And when it finally ended in 2019, ABB paid $55 million to settle the case, plus an estimated $50 million in legal defense costs. Total company exposure: $105 million.

Cutler’s name appears in every legal analysis, every law firm client alert, every case citation. Searchable forever. Not for what he did, but for what he failed to document.

“A trustee is held to something stricter than the morals of the marketplace. Not honesty alone, but the punctilio of an honor the most sensitive, is then the standard of behavior.”

— Justice Benjamin Cardozo

The court found he and the other defendants to be “jointly and severally liable.” That means Cutler could be personally on the hook for the full judgment. Whether ABB’s indemnification and insurance covered him completely, we don’t know. That’s an important point.

If you’re serving as a fiduciary, you better make sure you’re covered before you find out the hard way.

Why This Matters for Health Plans

Tussey v. ABB was a 401(k) case. But the law firm that brought it, Schlichter Bogard & Denton, has now turned its attention to health plans.

The voluntary benefits lawsuits they filed in December use the same playbook: allege fiduciary breach, demand documentation of the decision-making process, and let discovery do the rest.

The parallels are striking:

Comparison of 401(k) vs.Health Plan Breaches

What the Court Actually Found

The Eighth Circuit’s language was direct. The court found “strong evidence” Cutler “openly communicated with Fidelity about the ‘pricing implications’ of changes to the plans’ investment lineup.” His recommendation would generate more revenue sharing for Fidelity and reduce ABB’s hard-dollar costs.

The district court concluded: “ABB fiduciaries were not concerned about the cost of recordkeeping unless it increased ABB expenses.”

In other words: they prioritized company interests over participant interests.

The court saw “too many coincidences to make the beneficial outcome for ABB serendipitous.” The specific breaches included:

Failing to calculate dollar amounts paid through revenue sharing

Failing to benchmark recordkeeping fees

Failing to leverage plan size to negotiate lower costs

Allowing 401(k) plan assets to subsidize corporate services.

Two Questions That Would Have Saved Him

Two Questions

The Price of Not Asking

Two questions. He asked neither.

$105 million.

By The Numbers

The Questions They Will Ask You

If your health plan faces litigation, your fiduciaries will likely have to sit for a deposition. These are the kinds of questions plaintiffs’ attorneys ask, based on the 401(k) playbook.

For each one, know what they’re looking for and what your documented answer should be:

1. “Who authorized the formation of your benefits committee?”

What they’re looking for: Evidence of proper delegation from the board.

Your documented answer: Board resolution dated [X], copy attached as Exhibit [Y].

2. “Where is your written charter defining committee responsibilities?”

What they’re looking for: Documented scope of fiduciary authority.

Your documented answer: Fiduciary Committee Charter, adopted [date], last reviewed [date].

3. “Did each committee member acknowledge their fiduciary duties in writing?”

What they’re looking for: Evidence members understood their obligations.

Your documented answer: Signed acknowledgment letters from each member, dated upon appointment.

4. “Show me your meeting minutes from the past three years.”

What they’re looking for: Regular meetings with documented deliberation.

Your documented answer: Quarterly meeting minutes showing attendance, agenda items, discussions, and decisions.

5. “Who evaluated conflicts of interest?”

What they’re looking for: Process for identifying and managing conflicts.

Your documented answer: Conflict of Interest Disclosure forms collected annually, committee review documented in [date] minutes.

6. “Walk me through how you selected your vendor.”

What they’re looking for: Evidence of a prudent process, not just good outcomes.

Your documented answer: RFP documentation, vendor scorecards, committee deliberation notes, decision memo with rationale.

7. “How did you benchmark your pricing?”

What they’re looking for: Comparison to market rates, evidence fees are reasonable.

Your documented answer: Annual benchmarking report from [source], committee review documented in [date] minutes.

Your Legal Defense File

If you were sued tomorrow, could you produce this file? Editable templates for these documents can be found in the Fiduciary Handbook Fast Start Kit from Nautilus.

Editable Templates

1. Board Authorization Letter establishing the committee

2. Fiduciary Committee Charter defining scope and responsibilities

3. Acknowledgment Letters signed by each committee member

4. Meeting Minutes from at least the past three years

5. Conflict Disclosures from all advisors and committee members

6. Documentation showing your RFP process, scoring rubric, and decision rationale

7. Benchmarking Reports comparing your costs to market rates

1. Pull your legal defense file. Can you produce the seven documents listed above? If any are missing, download the templates and schedule time to create them. 2. Schedule your next committee meeting. If you haven’t met in 90+ days, get a date on the calendar. Document attendance, agenda, discussion, and decisions.

3. Locate your indemnification agreement. If you serve on a benefits committee, confirm in writing your employer indemnifies you for fiduciary claims. ERISA prohibits the plan from indemnifying fiduciaries, but the employer can.

4. Verify your fiduciary liability coverage. Call your broker Monday. Confirm policy limits, whether the plan or employer pays premiums, and whether a “no recourse” rider protects individual fiduciaries.

In Closing

John Cutler spent thirteen years as a defendant. Thirteen years of depositions, document requests, and legal strategy meetings. Thirteen years of having his professional judgment questioned in court filings.

His offense? He made a recommendation. It may or may not have been the right recommendation. But he could not prove he followed a prudent process to get there.

The plaintiff law firms perfected this playbook in 401(k) litigation and have now turned to health plans. The same questions are coming. The same documentation will be demanded.

The only question is whether you will be ready.

Until next week,

P.S. Don’t skip #3. “Do we have written indemnification for benefits committee members?” If the answer is “I think so” or “I’ll check,” remember: John Cutler probably thought he was covered too.

Next Week: Broker disclosure forms are designed to check a box, not answer your questions. We’ll fix that.

📤 Share: Forward this issue to your CEO, CFO, or General Counsel

💸 SPECIAL OFFER: Newsletter subscribers receive 10% off any Validation Institute service. Use code FIDUCIARY10 at checkout.

A Note of Appreciation

Julie Selesnick is the founder and principal attorney at Health Plan Legal Counsel PLLC and a key advisor to Nautilus Health. Julie is focused on providing legal and consulting services to health plans, vendors to group health plans, and other stakeholders in the ERISA and non-Federal governmental employer sponsored and Taft Hartley plans.

Don’t be a bystander. Change the status quo and reap the benefits of The Health Plan Compliance Advantage. Schedule an introductory call with us.