The Schlichter voluntary benefits lawsuits filed in December expose a two-part failure most employers share: fiduciaries skipped compensation disclosure requests, and when disclosure existed, they accepted the amounts without evaluating reasonableness.

That’s the allegation against United Airlines, Labcorp, Community Health Systems, and Allied Universal. Major consultancies are named as co-defendants: Mercer, Gallagher, Lockton, Willis Towers Watson. The claims center on voluntary benefits: accident, critical illness, and hospital indemnity insurance employees pay for entirely through payroll deduction.

But the disclosure gap extends well beyond voluntary benefits. If you’ve skipped demanding and evaluating disclosure for these products, have you done it for your broker? Your PBM? Your TPA? For most employers, the answer is the same.

The lawsuits are a preview of where scrutiny is heading.

Every Question Leads to Another Question

Start with a simple question:

Did my broker provide the compensation disclosure required by the Consolidated Appropriations Act?

Pull the document. If it exists, ask the next question:

Does it include voluntary benefits?

Many brokers claim voluntary benefits are “non-ERISA” and therefore exempt from disclosure. But if those same products appear on your Form 5500 Schedule A, you have a contradiction. The plan reported them. The broker omitted them. Plaintiffs’ attorneys will find that mismatch.

If voluntary benefits are disclosed, ask the next question:

Is the compensation reasonable compared to benchmarks?

The United Airlines complaint alleges 36% of premium went to commissions. Comparable programs cited by plaintiffs ranged from 2% to 19%. Major medical broker compensation typically runs 2% to 8%.

If the compensation seems high, ask the next question: What’s the commission structure?

Commissions are often “heaped” paying 60% to 75% in year one, then dropping to 10% to 20% in subsequent years. This structure creates an incentive to flip carriers every two to three years. Each flip resets the commission clock. The broker wins. The pattern continues.

This is what happens when you turn over rocks. Each question reveals something requiring explanation.

Turning Over Rocks

The Schlichter lawsuits are conducting this audit in discovery. The question is whether you’d rather conduct it yourself now, or have opposing counsel do it for you later.

Dave Chase, co-founder of Health Rosetta, described employers learning what their brokers actually earn as the “business equivalent of finding out your spouse was cheating on you.“

Some brokers argue voluntary benefits compensation falls outside CAA disclosure requirements because the products are “non-ERISA.” The argument reveals more than it intends.

Translation: I’ll disclose if the government compels me. Otherwise, I’d prefer you stay in the dark.

That’s a salesperson protecting revenue. It’s the opposite of a fiduciary advisor acting in your interest.

Here’s a simple test: Ask your broker for complete compensation disclosure across all products. Include voluntary benefits explicitly in your request. Note how they respond.

A broker operating as a true advisor welcomes the question. A broker operating as a salesperson deflects, delays, or carves out exceptions.

The response tells you everything about the relationship.

The Cross-Subsidy Problem

Some excess compensation may not flow directly to the broker’s pocket. It might offset other plan expenses. Fund “platform fees” or “panel fees” paid to access certain carriers. Even subsidize client entertainment.

This practice creates an ethical problem beyond overpayment.

Plan participant dollars, collected through payroll deduction, end up funding things benefiting the employer, the broker, or the carrier. Employees paying premiums are unaware their money subsidizes someone else’s glamorous travel junket.

The Tussey v. ABB 401(k) case established a related principle:

Plan fiduciaries can’t allow participant assets to subsidize corporate expenses, even when fees to the plan stay flat.

The appearance of benefit to employees doesn’t excuse the use of their dollars for other purposes. Voluntary benefits create similar exposure. Employees pay 100% of the premium. The employer’s role is facilitation and oversight.

When oversight fails, the people paying the premiums pay the price.

The Benchmark Challenge

Even if you ask, how do you evaluate? The voluntary benefits market has operated without much transparency. Benchmarks are scarce.

Here’s what the research shows:

Major medical broker compensation: 2% to 8% of premium is typical.

Fee-based advisor comparison: Advisors working on flat PEPM (per-employee-per-month) fees typically charge $5 to $15 PEPM. Compare this to what your commission-based broker makes. The math often reveals the gap.

Loss ratios: Higher is better for participants. A low loss ratio means more premium going to commissions and administration, less going to claims.

Transparent alternatives: Group captive models for voluntary benefits target 60% or more of premium going to claims, with any underwriting surplus returned to participant programs.

The absence of published benchmarks doesn’t excuse the absence of a prudent process. Document your methodology. Show your work. That’s what fiduciaries do.

What to Do First Thing Monday

Pull your broker’s CAA disclosure. Does it exist? Is it dated within the past twelve months? Does it include voluntary benefits? If any answer is no, request an updated, complete disclosure in writing.

Compare to Form 5500 Schedule A. If voluntary benefits appear on Schedule A but are absent from the broker’s disclosure, ask for an explanation. Document the response.

Ask when your voluntary benefits carrier last changed. If the answer is within the past two to three years, and the change before that was also recent, you may have a commission churn pattern. Request the commission structure in writing.

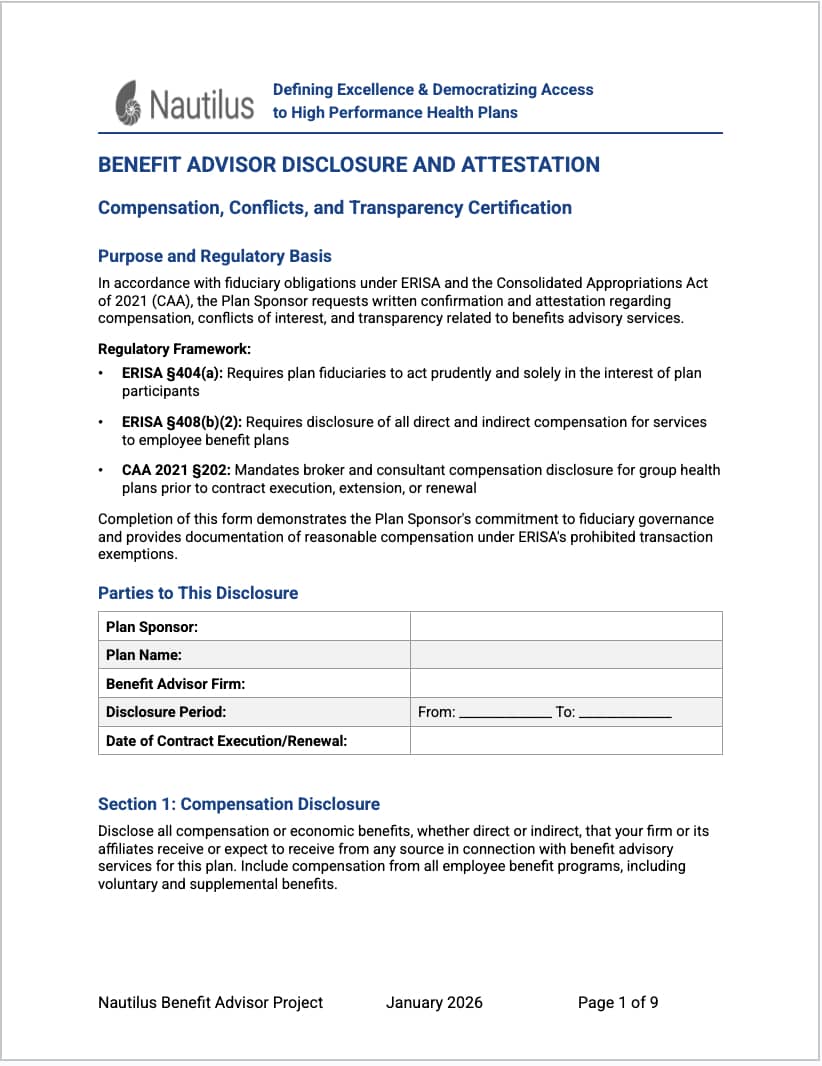

Request disclosure from every vendor receiving plan-related compensation. Brokers, PBMs, TPAs, stop-loss carriers. Use the Nautilus disclosure template below for the questions. Document what you asked and what you received.

Tools & Resources

Benefit Advisor Disclosure & Attestation

The foundation of each Nautilus project is developing standards defining what excellence looks like. Nautilus resources are free and openly available to any individual and organization to use.

Here’s the latest Nautilus Benefit Advisor Disclosure and Attestation form. You should download and use this editable template now but remember: the law requires you to receive disclosures “reasonably in advance” of each renewal.

In Closing

The Schlichter lawsuits aren’t about voluntary benefits specifically. They’re about disclosure and evaluation: the two steps fiduciaries are supposed to take and often skip.

Every vendor relationship deserves the same scrutiny now being applied to voluntary benefits. The questions are straightforward. The documentation is achievable. The alternative is explaining to a court why you never asked.

Your employees and their families pay premiums, deductibles, and copays. They trust the plan operates in their interest. That trust is earned through process: asking questions, evaluating answers, documenting decisions.

Here’s to clearer thinking, stronger plans, and better outcomes for the people who rely on us.

All the best,

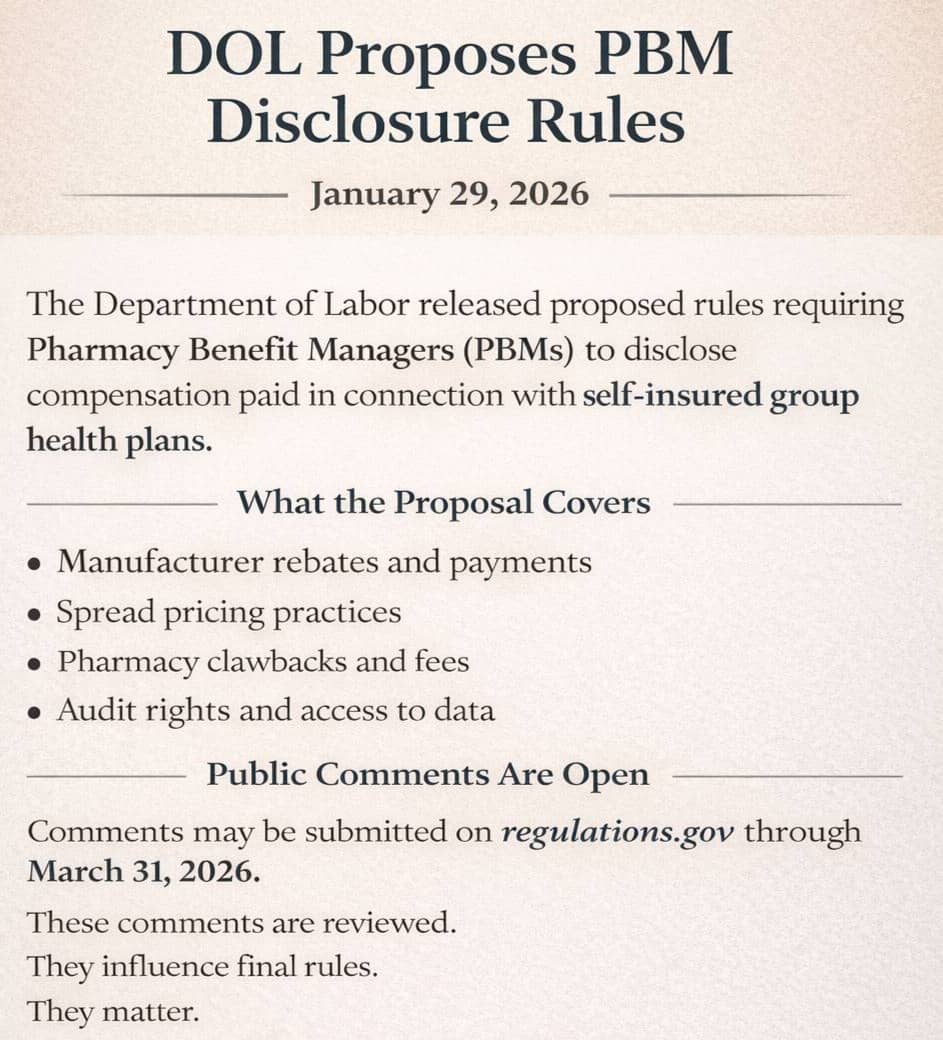

P.S. We got some good news from Washington late last week. On January 29, the Department of Labor proposed rules requiring PBMs to disclose compensation to self-insured group health plans.

DOL Proposed PBM Disclosure Rules

If your broker resists voluntary benefits disclosure and your PBM resists rebate transparency, the pattern is the same: disclosure requirements keep expanding because voluntary transparency keeps failing.

Subscribe & Share

🔗 Subscribe: Was this newsletter forwarded to you? Signup to receive The Health Plan Compliance Advantage every Monday.

📤 Share: Forward this issue to someone wrestling with broker disclosure or voluntary benefits oversight.

💸 SPECIAL OFFER: Newsletter subscribers receive 10% off any Validation Institute service. Use code FIDUCIARY10 at checkout.

────────────────────────────────────────

A Note of Appreciation

Dave Chase, is the co-founder of Health Rosetta and Nautilus Health Institute, a 501(c)(3) nonprofit launched with $4 million in Health Rosetta intellectual property and investment. Dave has seen every sort of “health plan shenanigans” and created Nautilus to establish open-source standards, model contracts, and data platforms to make fairness, accountability, and measurable outcomes the new norm in healthcare.

Don’t be a bystander. Change the status quo and reap the benefits of The Health Plan Compliance Advantage. Schedule an introductory call with us.