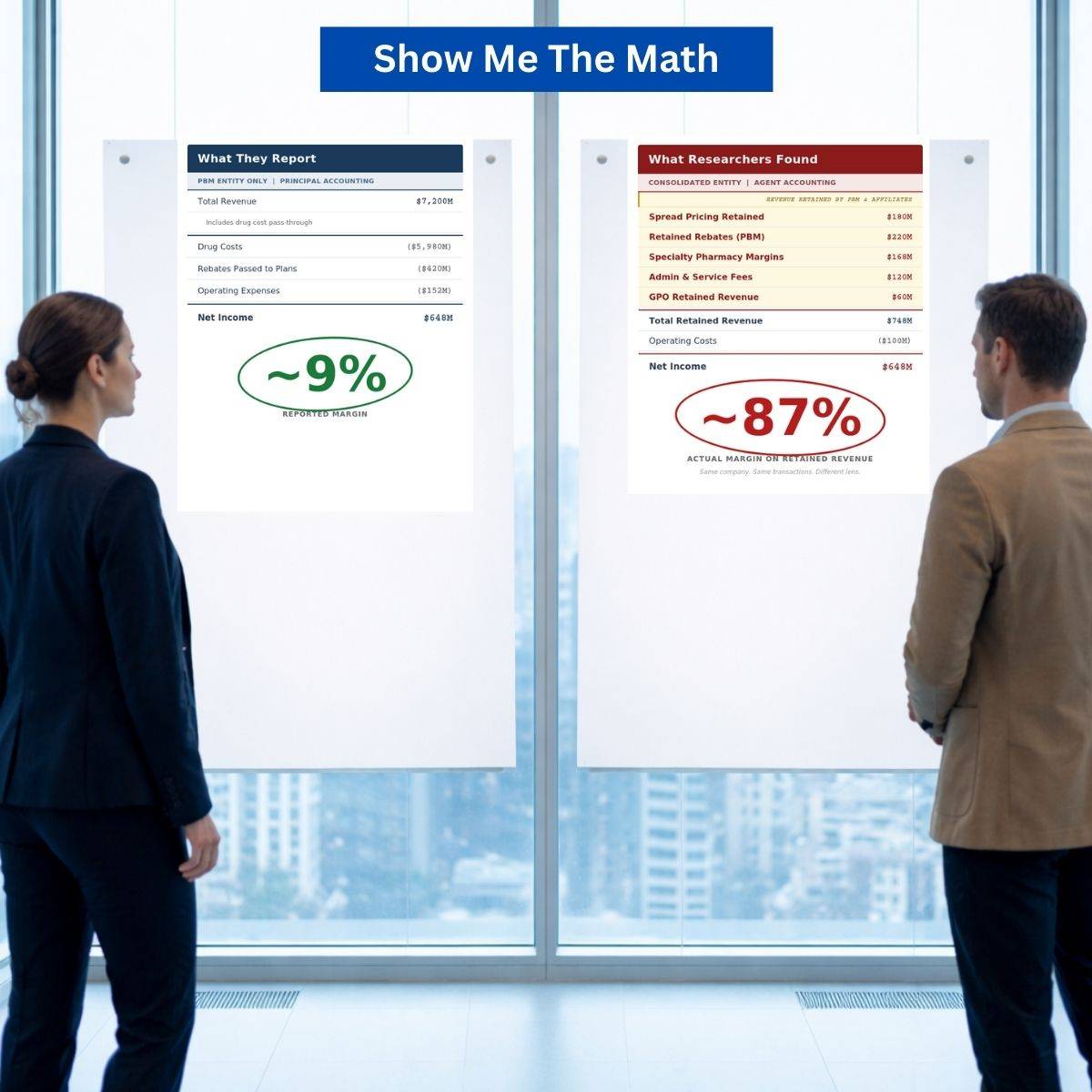

What would you do if you were told your PBM earned a 9% margin and researchers found the real number could be closer to 87%?

That’s not a hypothetical. A USC Schaeffer Center white paper published in January showed PBM profit margins on the same drug can range from 9% to 87% depending on how the PBM accounts for pass-through payments and internal transfers within its parent company.

The DOL just proposed a rule to cut through that fog and other pricing shell games. They want to hear from the employers who pay the bills. Comments close March 31.

Whiteboard With Margin Calculations

Executive Brief

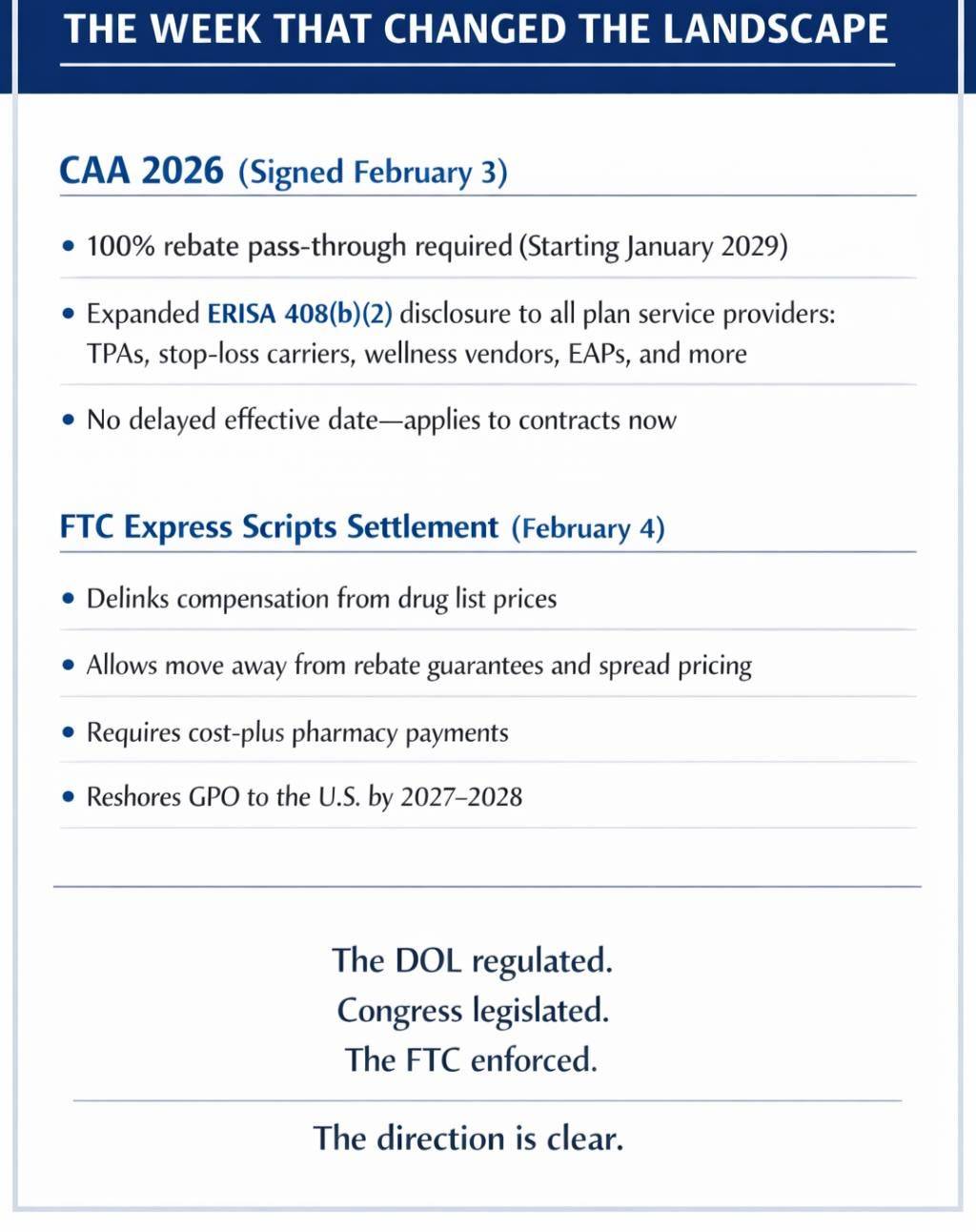

The DOL’s proposed rule was one of three separate federal actions on PBM transparency in a single week. On February 3, the President signed CAA 2026 into law, mandating 100% rebate pass-through. On February 4, the FTC settled with Express Scripts, requiring structural overhaul of how the largest PBM prices drugs and reports to plan sponsors.

This issue focuses on the DOL rule because it comes with something the others do not: an open invitation for employer input. The people writing this standard want to hear from the fiduciaries who live with PBM contracts every day. That opportunity closes in six weeks.

What the DOL Rule Means for You

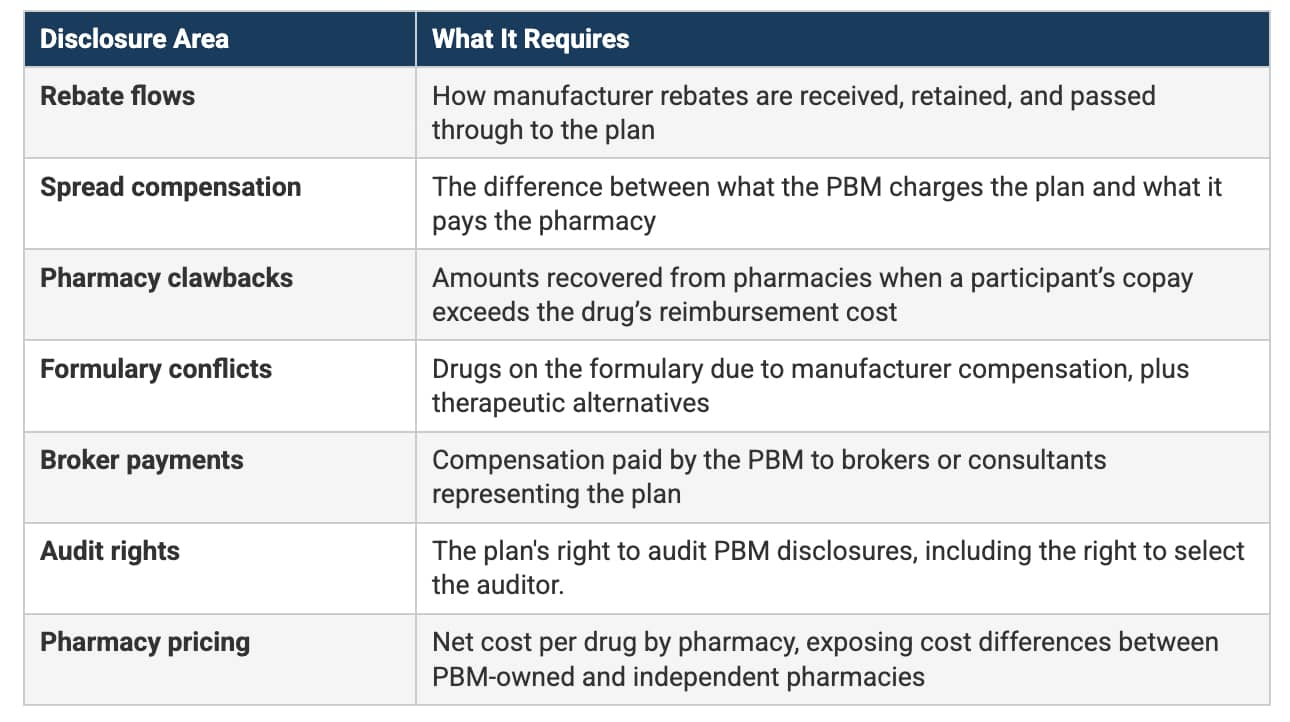

The proposed rule uses the existing ERISA 408(b)(2) framework, the same structure already in place for retirement plan service providers. It requires PBMs serving self-insured ERISA plans to disclose:

PBM Disclosure Rules

One important clarification: this is a disclosure rule. It tells PBMs to show you what they earn. It does not tell them to stop earning it. CAA 2026 handles the prohibition side (see sidebar). The DOL rule creates the transparency that lets you evaluate whether your arrangement is reasonable. That evaluation is the fiduciary’s job.

The Week That Changed The Landscape

What the Industry Is Saying

We reviewed commentary from employer coalitions, benefits attorneys, and industry analysts. The consensus is striking: everyone agrees the rule is a strong foundation. We found no one recommending any provision be weakened or removed.

The discussion centers on where the rule should go further. Here are the areas getting the most attention, and the ones where your comments will have the greatest impact.

Close the GPO Affiliate Loophole

This is the gap cited most often. All three major PBMs own group purchasing organization subsidiaries that negotiate rebates with drug manufacturers. These GPOs can retain a portion of the rebates before passing the remainder to the PBM. Because the DOL rule requires disclosure at the PBM level, a PBM could report 100% pass-through while the parent company keeps revenue through its GPO.

Multiple legal analyses flagged this. The USC Schaeffer white paper documented how vertical integration allows dollars to shift between business units as internal transfers invisible to the public: the publicly reported profit margin can be half of what the company records internally. And as one attorney noted, PBMs have shifted rebate negotiation functions to affiliated GPOs specifically to move revenue outside standard reporting and contractual pass-through obligations. The revenue did not disappear. It was reclassified and routed through entities that fall outside the reporting requirements.

What to say: Urge the DOL to require consolidated reporting at the parent entity level, covering all affiliates involved in the prescription drug supply chain.

Standardize the Reporting Format

The ERISA Industry Committee (ERIC) recommended the DOL develop a common reporting template so fiduciaries can digest data and compare disclosures across PBMs. Without a standard format, each PBM will report differently, making comparison nearly impossible. This is a practical concern employers are uniquely positioned to raise.

What to say: The DOL should create or adopt a standardized disclosure template. Fiduciaries need the ability to compare PBM compensation across vendors in a consistent format.

Strengthen Audit Rights

The proposed rule includes audit provisions, which is welcome. It also specifies audit costs be split 50/50 between the plan and the PBM. That deserves pushback. The audit verifies the accuracy of the PBM’s own disclosures. Requiring the plan to subsidize the PBM’s cost of cooperating creates a financial disincentive to exercise audit rights. The standard commercial approach is simpler: each party bears its own costs of conducting the audit.

What to say: Push for no PBM restrictions on auditor selection or methodology, annual audit frequency at minimum, each party bearing its own costs, and the ability to extrapolate findings.

Address Data Ownership

The rule requires PBMs to disclose compensation but says nothing about plan sponsor access to the underlying claims data. Transparency without data access is incomplete. A fiduciary cannot independently verify PBM disclosures, conduct meaningful audits, or evaluate alternative arrangements without unrestricted access to their own plan’s data.

What to say: The final rule should affirm plan data belongs to the plan, not the PBM. Fiduciaries should have unrestricted access to claims-level data in usable formats, with the right to share that data with auditors, consultants, and alternative vendors without PBM consent.

Coordinate the Effective Dates

The DOL rule could take effect as early as mid-2026. CAA 2026 PBM provisions arrive January 2029 for calendar year plans. Several commentators noted the DOL will need to harmonize these timelines to avoid conflicting requirements during the transition period.

What to say: Support the earliest possible effective date for DOL disclosure requirements. Employers need this information now, and waiting three years for CAA 2026 implementation is too long.

The attached comment strategy document covers three additional areas including termination rights, indemnification, and pricing model disclosure. Download and share with your team.

A Note on Fully Insured Plans

The rule covers self-insured ERISA plans only. The DOL explicitly requested comments on extending to fully insured arrangements, and many commentators have urged extension. Ranking Member Bobby Scott called the narrow scope a missed opportunity.

We share the goal. Participants in fully insured plans deserve the same protections. But the path matters. Fully insured plans sit primarily under state insurance regulation, and 26 states enacted PBM legislation in 2025 alone, many covering fully insured arrangements. A broad federal mandate could preempt stronger state protections in some jurisdictions, or create enough legal complexity to delay finalization for the self-insured plans that clearly need it now.

If you support extension in your comments, they will carry more weight if they acknowledge this complexity and propose a workable approach.

The pragmatic path may be to get the self-insured framework right first, then extend carefully so federal requirements complement rather than conflict with state protections already in place.

From Disclosure to Decision

The DOL rule delivers the disclosure. The fiduciary still has to deliver the decision.

The industry is celebrating transparency. Rightly so. But receiving a disclosure is only half the equation. The fiduciary cases working through the courts right now are built on a two-step failure: employers who never asked for information, and employers who received information but never evaluated whether the arrangement was reasonable.

The DOL rule addresses the first step. It gives fiduciaries the right to see PBM compensation. But having the data in hand does not satisfy fiduciary duty. You still need a documented process for evaluating what the data tells you, comparing it to alternatives, and making a reasoned decision about whether to continue, renegotiate, or replace.

Transparency puts numbers on the table. Accountability means someone reviews them, documents the review, and acts on what they find.

What to Do First Thing Monday

Review the attached comment strategy and identify which recommendations reflect your plan’s experience. We have attached a sample employer comment letter and a recommended comment strategy document to this issue. Use them as starting points. The DOL specifically asked to hear from plan sponsors, and comments grounded in real fiduciary experience carry the most weight. Instructions for submitting are included.

Add the DOL proposed rule to your next fiduciary committee agenda. If you have a health plan committee (and you should), this is exactly the kind of item that belongs on the agenda. Document the discussion. A committee decision to review and respond to the proposed rule is a fiduciary action worth recording.

Forward this issue to your CEO, CFO, or General Counsel. The March 31 deadline is a leadership moment. Public comments from plan fiduciaries carry more weight than comments from industry lobbyists. Your executive team should know the opportunity exists.

Nautilus Tools and Resources

Here are some downloadable tools you can use. Share the Comment Strategy document wth your fiduciary committee and leadership. Use the Sample Comment Letter to guide development of your comments.

Customizable letter template for plan fiduciaries to submit before March 31.

In Closing

The DOL opened a door and asked employers to walk through it. The people writing this rule want to hear from the fiduciaries who manage prescription drug benefits for millions of working Americans and their families.

Six weeks remain. Use them to your advantage.

Here’s to clearer thinking, stronger plans, and better outcomes for the people who rely on us.

All the best,

P.S. Next month: the contract standards framework we have been developing with national employer coalitions. If the DOL rule tells you what your PBM earns, the framework helps you decide what to do about it.

Subscribe & Share

🔗 Subscribe: Was this newsletter forwarded to you? Signup to receive The Health Plan Compliance Advantage every Monday.

📤 Share: Forward this issue to someone wrestling with PBM oversight.

💸 SPECIAL OFFER: Newsletter subscribers receive 10% off any Validation Institute service. Use code FIDUCIARY10 at checkout.

────────────────────────────────────────

A Note of Appreciation

Shawn Gremminger

Shawn Gremminger is President and CEO at the National Alliance of Healthcare Purchaser Coalitions.

Shawn and his team, the coalitions and their leadership, and many individual contributors deserve congratulations and thanks for persevering over many years to pass the most meaningful PBM reform in a generation.

Don’t be a bystander. Change the status quo and reap the benefits of The Health Plan Compliance Advantage. Schedule an introductory call with us.