Cigna’s CEO Told Wall Street PBM Reform Won’t Affect Profits

Executive Brief

On February 3, 2026, President Trump signed the Consolidated Appropriations Act (CAA) of 2026 into law. The legislation includes the most comprehensive federal PBM reform package ever enacted. 100% rebate pass-through. Spread pricing prohibitions. Expanded ERISA 408(b)(2) disclosure requirements. Semi-annual reporting. Enforcement penalties of $10,000 per day.

This is a generational win for the employer coalitions, pharmacy advocates, legislators, and countless individuals who made this happen. Full stop.

Here is the problem with celebrating too long: the major provisions take effect January 1, 2029. Three years from now. And between today and that date, every PBM in the country will be restructuring its business model.

In fact, Cigna’s CEO has already told Wall Street PBM reform won’t affect profits. Read that again.

If you wait until 2029, you will inherit whatever model your PBM designs to replace the one Congress just outlawed. The question is whether you shape the transition or absorb it.

What Actually Passed

The PBM provisions in CAA 2026 address the core issues employer advocates have raised for years. Here is a summary of the key reforms:

Compensation Structure Overhaul

PBMs must remit 100% of rebates, fees, alternative discounts, and all manufacturer remuneration to plan sponsors. Quarterly remittance is required within 90 days. PBM compensation shifts to flat administrative fees for bona fide services. Plan sponsors gain explicit audit rights, with the auditor chosen by the plan fiduciary. The PBM cannot pay for the audit, directly or indirectly.

Expanded Disclosure Requirements

PBMs are now included as covered service providers under ERISA 408(b)(2). Semi-annual reporting is required (quarterly upon request) covering claim-level, drug-level, rebate-level, and pharmacy-level data. PBMs must disclose compensation flows, spread reporting, formulary placement rationale, and affiliate pharmacy incentives. Summary documents must be available to individual participants and beneficiaries upon request.

Enforcement with Teeth

Civil monetary penalties reach $10,000 per day for non-compliance and $100,000 for knowingly providing false information. If a PBM violates the rebate requirements, its contract becomes “unreasonable” under ERISA Section 408(b)(2)(B), constituting a prohibited transaction. Plan sponsors can seek reimbursement from PBMs for penalties incurred due to PBM non-compliance.

Implementation Timeline

Effective date: Contracts entered into, extended, or renewed for plan years beginning 30 months after enactment. For calendar year plans, this means January 1, 2029. HHS to deliver standard reporting formats by mid-2027.

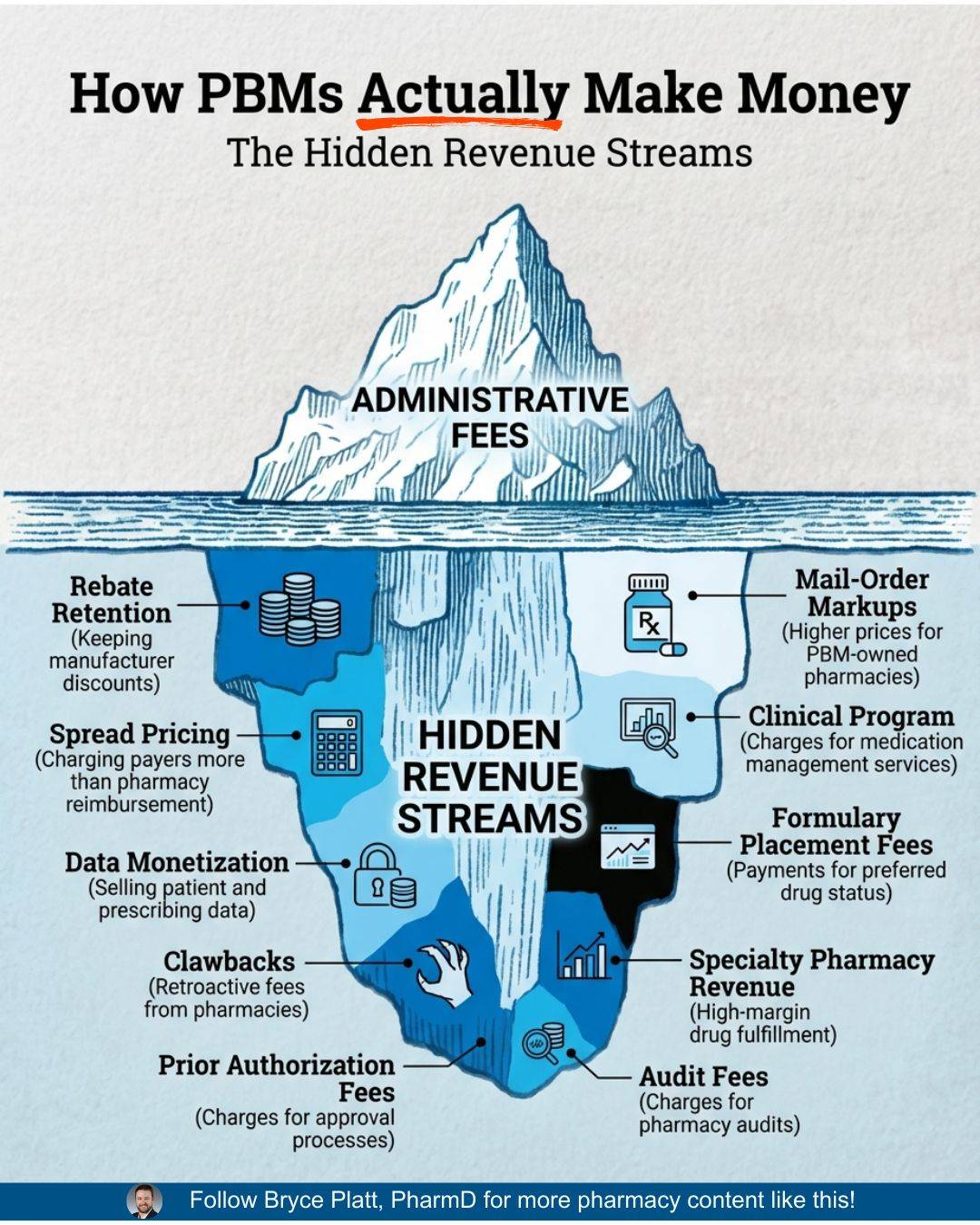

The Iceberg: Admin Fees Are Just the Surface

Pharmacist and PBM consultant Bryce Platt recently published an image worth studying. It shows an iceberg. Above the waterline: admin fees. Below the waterline: ten other revenue streams PBMs use to monetize their position between employers, pharmacies, and manufacturers.

PBM Iceberg Courtesy of Bryce Platt

The image is striking because it makes visible what most employers have never mapped. Admin fees are the one line item plan sponsors see clearly. They only represent a portion of how many PBMs generate revenue.

Below the waterline, the picture gets far more complex: spread pricing, DIR fees, pharmacy clawbacks, manufacturer rebates retained through affiliate arrangements, specialty drug markups, mail-order steering incentives, formulary placement fees, utilization management fees, data licensing revenue, and more.

Congress just banned a few of the items below the waterline. The iceberg above and below the surface is going to shift and grow.

This is the core challenge of CAA 2026 implementation. The law addresses specific practices. PBMs operate a portfolio of revenue streams. When one gets restricted, others expand.

This pattern is what some call a shell game. We like to think of it as “whack-a-mole.”

If It Won’t Affect Profits, Where Does the Money Come From?

Two days after President Trump signed CAA 2026 into law, Cigna CEO David Cordani held an earnings call with Wall Street analysts. Cigna owns Express Scripts, one of the three largest PBMs in the country.

Cordani’s message to investors was clear: the PBM reform law will have no material impact on Express Scripts’ profitability. The company is “well positioned to execute.” The stock rose 3% on the news.

Read those two statements together. Congress passed the most comprehensive PBM reform legislation in a generation. The CEO of a company most directly affected told Wall Street: our profits are safe.

If the law bans the practices that generated the profits, and the profits stay the same, the money is coming from somewhere.

Cordani described the convergence of legislation, regulation, and the FTC settlement as a “clearing event” the company has long anticipated. Express Scripts plans to market its new rebate-free model with “aggressive adoption.” Cigna projects $280 billion in revenue for 2026.

This is the clearest signal employers will receive. The PBMs are telling their investors, explicitly and on the record, the reforms will be absorbed without affecting the bottom line. That means the revenue currently generated through spread pricing, rebate retention, and the practices Congress just restricted will be replaced. The iceberg below the waterline is the replacement plan. Plus some new ones you may have not thought about.

Six Ways PBMs Will Adapt (and How to Prepare Now)

PBMs are sophisticated financial operations. They will comply with the law. They will also restructure to preserve revenue. Here are six adaptation strategies to anticipate and address in your next contract:

1. Recharacterized Spread Pricing

Spread pricing in its traditional form is prohibited. The transaction where a PBM charges the plan one price and pays the pharmacy a lower price will be explicitly visible. Expect new transaction structures, new terminology, and new ways to create distance between what the plan pays and what the pharmacy receives. Your contract should define spread pricing broadly enough to capture any differential the PBM retains from the drug transaction, regardless of how it is characterized.

2. Post-Adjudication Intensification

Pharmacy clawbacks, Direct and Indirect Remuneration (DIR) fees, and retroactive pricing adjustments represent a second category of extraction. If upfront spread becomes impermissible, the back end of the transaction becomes an attractive extraction mechanism. Your contract should prohibit all post-adjudication adjustments retained by the PBM and require full pass-through of any pharmacy recoveries to the plan.

3. Administrative Fee Inflation

This is the most predictable adaptation. CAA 2026 explicitly permits “bona fide service fees” that are flat, transparent, and tied to services actually performed. Expect admin fees to increase significantly as PBMs repackage revenue previously captured through spread and rebate retention. The question is whether those fees reflect the actual cost and value of services provided. Your procurement process should benchmark admin fees across multiple vendors and require detailed fee schedules tying each fee to a specific, measurable service.

4. Utilization Management Monetization

PBMs increasingly charge separately for clinical programs: prior authorization, drug utilization review, and specialty management. When the PBM profits from managing utilization, the conflict runs in two directions.

First, over-management. Every prior authorization and clinical review generates a touchpoint the PBM can bill for. The question is whether every prescription truly requires that level of review, or whether the process itself has become a revenue stream. When members face abrading processes at every turn, some give up. That serves the PBM’s economics, not the participant’s health.

Second, under-management with steering. A PBM approves every specialty drug prescribed, but routes it through owned channels: their biosimilar instead of the physician’s choice, their specialty pharmacy, their affiliated infusion center. The utilization management program becomes a funnel for directing volume to entities the PBM profits from, rather than a clinical safeguard for the plan.

Both directions represent conflicts of interest. Your contract should require complete transparency in utilization management fees, define the clinical criteria governing each review program, and evaluate whether the PBM’s compensation structure incentivizes appropriate care or revenue generation through its own affiliates.

5. Formulary Management Conflicts

Vertically integrated PBMs can manufacture or distribute their own biosimilars, specialty drugs, and generic products. When a PBM manages your formulary while also profiting from the products it places on the formulary, the conflict is structural. As rebate-based compensation declines, formulary placement becomes a more valuable revenue lever. Your contract should require disclosure of all affiliate products on the formulary, the financial benefit the PBM derives from each, and independent clinical justification for every formulary decision.

6. Vertical Integration Expansion

Some states are moving to restrict PBMs from owning pharmacies. The response may be expansion into adjacent care delivery: infusion centers, specialty clinics, oncology practices, and other high-cost care settings. If a PBM controls where specialty drugs are administered and profits from the administration, the steering incentive persists in a new form. Your procurement evaluation should map the PBM’s full corporate structure, including all owned or affiliated care delivery entities, and assess whether patient steering provisions adequately protect participants.

Every one of these adaptation strategies is preventable through disciplined procurement and the selection of a PBM with aligned incentives. The vendors operating under pass-through models with no vertical conflicts exist today. They existed before this law passed.

The law simply made the alternative model the eventual minimum standard.

“No Immediate Action Required” Is the Wrong Message

Within days of CAA 2026 becoming law, several major benefits consulting firms published guidance to their clients. The consistent message: no immediate action is required. Employers should prepare for contract restructuring, but there is nothing to do right now.

This passive guidance is comforting and wrong.

Here is what “no action required” actually means: for the next three years, your current PBM will redesign its compensation model, restructure its affiliate arrangements, repackage its fee schedules, and present you with a new contract in 2028 that technically complies with the law.

You will evaluate the new terms under time pressure, with limited visibility into what changed and why. You will rely on the same broker who placed your current arrangement to advise you on the new one.

That is a passive posture. It hands the transition to the party with the least incentive to protect your participants.

Three years is exactly the amount of time a PBM needs to build a compliant business model that preserves its revenue. Three years is also exactly the amount of time an employer needs to find a better one.

The employers who act now will select PBMs already operating under pass-through models with transparent compensation, aligned incentives, and no vertical conflicts.

They will lock in favorable terms before the 2029 deadline creates a procurement bottleneck.

They will have two to three years of claims data demonstrating the value of the new arrangement before their peers even begin the transition.

The employers who wait will get the model their PBM designs for them.

The DOL Proposed Rule: A Second Front

Four days before the President signed CAA 2026, the Department of Labor published a proposed rule expanding PBM disclosure requirements under ERISA. The proposed rule would require PBMs and affiliated brokers and consultants to disclose compensation information to fiduciaries of self-insured group health plans, including:

Rebates and other payments from drug manufacturers

Compensation received when the price paid by the plan exceeds the amount reimbursed to the pharmacy (spread)

Payments recouped from pharmacies (DIR fees and clawbacks)

Audit provisions allowing fiduciaries to verify the accuracy of disclosures

Public comments are due March 31, 2026. This is an opportunity for employers to shape the final rule. Your voice should be part of the record. Now is the time for employer comments.

The DOL rule and CAA 2026 are complementary. The legislation mandates specific PBM behaviors. The rule creates the disclosure framework fiduciaries need to verify compliance and evaluate reasonableness.

Together, they establish both the standard and the measurement tool.

What to Do First Thing Monday

Start preparing your DOL public comments. The proposed PBM fee disclosure rule will shape the regulatory framework for years. Employer input is specifically requested and the comment period closes March 31, 2026. Make your voice part of the record.

Send your incumbent PBM a Compliance RFI. Ask your current PBM to respond, in writing, to Nautilus Core Fiduciary Alignment Contract Standards. These 10 fiduciary-aligned contract provisions are consistent with CAA 2026 requirements and the DOL proposed disclosure standards. This accomplishes two things: it tests whether your incumbent can meet the standard the law will require, and it creates a documented record of fiduciary diligence. If they push back on terms Congress just mandated, that response tells you everything you need to know about the next three years.

Request proposals from a PBM already operating under these standards. Nautilus maintains a vetted short list of PBMs who have attested to model contract terms aligned with CAA 2026 requirements: pass-through pricing, full rebate remittance, transparent fees, unrestricted audit rights, and no vertical conflicts. These vendors already operate under the standard Congress set for 2029. Contact us for the current list. If you or your PBM believes it belongs on the list, we welcome their attestation. Send them our way for review.

In Closing

CAA 2026 validates what fiduciary-aligned employers have been doing for years. The law codifies the standards these employers already demanded in their contracts. For them, January 2029 changes nothing. They are already there.

For everyone else, the clock started on February 3. The PBMs know it. The question is whether you’ll use the same three years they will.

The iceberg below the waterline is real. The levers PBMs can pull extend far beyond the practices Congress addressed.

Disciplined procurement, transparent vendor selection, and aligned incentives are the only reliable protection. They were the right answer before this law passed. They are the urgent answer now.

Here’s to clearer thinking, stronger plans, and better outcomes for the people who rely on us.

All the best,

P.S. Study the iceberg image from Bryce Platt closely. Count the revenue streams below the waterline. Then ask your PBM one question: “Which of these do you use, and which will you add when your current revenue streams are restricted?”

Next Week

The DOL proposed rule deserves a deep dive. We’ll break down the specific disclosure requirements, what they mean for your PBM relationship, and how to structure a public comment that advances employer interests. The March 31 deadline is closer than it looks.

Subscribe & Share

🔗 Subscribe: Was this newsletter forwarded to you? Signup to receive The Health Plan Compliance Advantage every Monday.

📤 Share: Forward this issue to someone wrestling with broker disclosure or voluntary benefits oversight.

💸 SPECIAL OFFER: Newsletter subscribers receive 10% off any Validation Institute service. Use code FIDUCIARY10 at checkout.

────────────────────────────────────────

A Note of Appreciation

Bryce Platt, PharmD is a healthcare strategist bridging the clinical, financial, and policy dimensions of U.S. pharmacy.

Bryce is a valued contributor to the Nautilus PBM Project and developed the Curated List of PBM Studies in our Executive Thought Leadership library.

Don’t be a bystander. Change the status quo and reap the benefits of The Health Plan Compliance Advantage. Schedule an introductory call with us.