And Why Fiduciaries May Not Have a Choice Much Longer

Executive Brief

Rebates have become the duct tape holding together an increasingly dysfunctional pharmacy benefit market.

They prop up premiums, pad budgets, and help employers keep annual renewals from looking less unhinged than they really are.

But here’s the uncomfortable truth:

Rebates don’t magically appear. Your sickest employees generate them.

That makes rebates more than a clever financing mechanism.

It’s a fiduciary dilemma.

One that Cigna’s newly announced “rebate-free pharmacy model” just blasted back into the spotlight.

And once you see the problem clearly, it’s hard to unsee it.

Because the people suffering the most physically are paying the most financially and subsidizing everyone else.

That’s the trap. And fiduciaries won’t be able to ignore it much longer.

What Cigna Just Announced (And Why It Matters)

Cigna’s Evernorth (Express Scripts) unit announced a new pricing model that embeds rebates directly into point-of-sale pricing instead of collecting them on the back end and redistributing them later.

If it works as advertised, it would:

Lower out-of-pocket costs

Create more predictable pricing

Shrink the gross-to-net bubble

Reduce PBM steering toward the highest-rebate drugs

Make the transaction cleaner, simpler, and harder to game

So why won’t employers rush to adopt it?

Because rebates are the third rail of pharmacy benefits:

They subsidize premiums

They disguise true costs

They smooth out budgets

And they let employers pretend the system is working “well enough”

Rebates feel like free money. But they’re not free. They’re extracted from somewhere.

Where Rebates Actually Come From

Mark Cuban has been saying this part out loud for a while now:

“Every CEO loves those fat rebate checks. ‘Oh, that goes on my balance sheet. That looks so good.’ But here’s what you don’t see: Your employees are rationing insulin, skipping cancer meds, and choosing between groceries and prescriptions while you cash rebate checks funded by their suffering.”

– Mark Cuban

He’s absolutely right. Rebates aren’t a discount.

They’re a transfer from the high-acuity few to the low-acuity many.

These sick employees carry the financial burden.

Their dollars produce the rebates.

Their conditions generate the “savings”.

And who benefits?

Often, everyone except them.

Healthy employees with minimal claims get lower premiums and more stable plan costs.

The sickest employees subsidize the entire group while the healthiest pay the least.

From a group-insurance standpoint, this isn’t new.

From a fiduciary standpoint, it’s radioactive.

Because ERISA doesn’t ask whether something “helps the group.”

It asks whether the plan sponsor is acting solely in the interest of participants including the ones who are sick, vulnerable, and financially exposed.

Today, the rebate system fails that fiduciary test far too often.

Mark Cuban

Why Employers Stay Stuck in the Rebate Trap

Most plans can’t imagine walking away from rebates.

Not because they don’t understand the dysfunction, but because:

They rely on rebates to buy down premiums

They’ve designed benefits around rebate inflows

CFOs budget with rebate guarantees

Brokers and PBMs reinforce the status quo

Specialty rebates provide outsized dollars

Any shift threatens to expose true costs

The result?

Even when a new rebate-free model promises fairness, transparency, and better alignment only a fraction of plan sponsors will adopt it.

Rebates became the crutch. Plan sponsors became dependent.

And dependency always feels like strategy until someone asks you to defend it in court.

Rebates Have Become The Opioid Of Pharmacy Benefits

The Fiduciary Risk No One Is Talking About

Here’s the real problem:

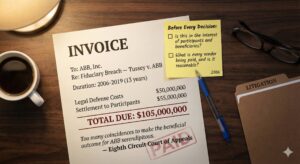

As lawsuits multiply and contract audits pick up steam, plaintiffs’ lawyers have discovered the rebate cross-subsidy.

And they’re asking the same question patients are:

“Why is the person with multiple sclerosis or cancer paying the most and producing the biggest rebates, only to have their money used to subsidize healthier employees?”

There’s no safe answer.

Not one that satisfies ERISA.

Not one a judge will like.

If PBM contracts and plan designs show rebates were used to lower premiums for the group while high-cost specialty users continued to face steep out-of-pocket burdens that’s an exposure.

A real one.

This is the first time the rebate cross-subsidy is being framed as a breach of loyalty.

And that changes everything.

What Fiduciaries Should Do Now

Reform doesn’t require adopting new models tomorrow.

But it does require breaking with the reflexive dependence on rebate economics.

Here are the steps to take now:

1. Demand Full Rebate Transparency

You can’t manage what you can’t see.

Require rebate reporting by drug, by class, and by member impact.

Audit rebate retention.

Follow the dollars.

If you can’t track it, you can’t defend it.

2. Model Pass-Through Scenarios

Use your data.

What happens to premiums if rebates flow to the point of sale?

What happens to out-of-pocket costs for your sickest members?

Model both. Compare both. Document both.

3. Redesign Cost-Sharing for Fairness

If your highest-acuity members are producing the value, they shouldn’t carry the steepest financial load.

That’s a fiduciary responsibility, not a design preference.

4. Update Your PBM Contract Language

Add provisions that:

Focus procurement on lowest net cost drugs

Allow you to adopt rebate-free or cost-plus pricing structures

Mandate reporting, audit rights, and extrapolation

Separate specialty rebates from premium subsidies

5. Put Rebates On the Fiduciary Governance Calendar

Rebate strategy shouldn’t be a once-a-decade conversation.

It’s an annual fiduciary checkpoint.

Document the rationale.

Document alternatives.

Document why you stay or shift.

The Bottom Line

Rebates have become the opioid of pharmacy benefit financing. They’re addictive, numbing, and impossible to quit without discomfort.

But fiduciaries don’t get to choose the easy path.

They choose the compliant path.

The defensible path.

The participant-first path.

Because when you discover a system where the sickest employees pay the most and end up subsidizing everyone else the only fiduciary response is to change it.

And that change needs to start now.

Note of Appreciation

Mark Cuban

Mark Cuban is the founder of Cost Plus Drugs and an outspoken advocate of change in pharmacy benefits. He has strong words for CEOs and the actions they need to take:

“Your PBM rebates aren’t savings. They’re a tax on your sickest employees. Every day you do nothing, you’re choosing profits over people. Fix it.”

Visit nautilushealth.org/pbm to find educational resources, procurement tools, model contract terms, the PBM Configurator, and other tools.

💸 SPECIAL OFFER: Newsletter subscribers receive 10% off any Validation Institute service. Use code FIDUCIARY10 at checkout.

validationinstitute.com

📬 PAY IT FORWARD: Feel free to forward this offer to your broker, PBM, or other vendors. Don’t hesitate to tell them you will favor validated vendors as part of your modernized procurement processes. Strong compliance and better benefits begin with validation.

Don’t be a bystander. Change the status quo and reap the benefits of The Health Plan Compliance Advantage.