You haven’t been happy with your PBM and think you found a better one. Pricing is materially better. The service model fits your plan. The references check out. Your advisor has the implementation plan ready.

Then your incumbent shows you the termination section of your current contract.

A wind-down fee, calculation method not stated. Notice required twelve months before the contract end date. Earned rebates forfeited if you exit before the end of the plan year. A pricing adjustment on the medical side if you change pharmacy vendors.

You do the math. Switching costs more than staying for another year. So you stay.

That is not a negotiation outcome. That is a PBM’s contract working exactly as designed.

This is the third provision in a three-part series. Issue 74 asked whether you can verify what your PBM is doing. Issue 75 asked whether you can act on what you find. This week: whether you can leave when you need to.

The Two-Test Standard

A fiduciary cannot evaluate a termination provision by reading it in isolation. The question is not whether a fee exists or how much notice is required. The question is whether the exit cost is fully disclosed before signing and whether the cost is reasonable in light of what the PBM is actually entitled to recover.

Two tests.

Test 1: Disclosure. Termination costs, if any, are quantified or calculable from the contract terms before signing. A fiduciary can sit at the bid table and compare the cost of exit across vendors with certainty.

Test 2: Reasonableness. Termination costs, if any, tie to stated up-front investment with amortization, or to defined wind-down work. They do not recover lost profits. They do not take accrued plan assets. They do not punish the plan for engaging another vendor.

A contract passes both tests when the cost of leaving is known and tethered to a legitimate expense. A clean example exists in the database: a wind-down fee structured as unamortized integration cost, reduced by 1/36 for each month elapsed since execution. The number is calculable on day one. It declines on a schedule. It reaches zero at term end. A fiduciary can defend the decision either way.

A contract fails one or both tests when the cost of leaving is hidden, when the cost has no basis in actual investment, or when the cost operates as a penalty regardless of how it is labeled.

The Five Patterns That Fail

Across the active contracts in the Contract X-Ray database, five recurring patterns appear in contracts that fail one or both tests:

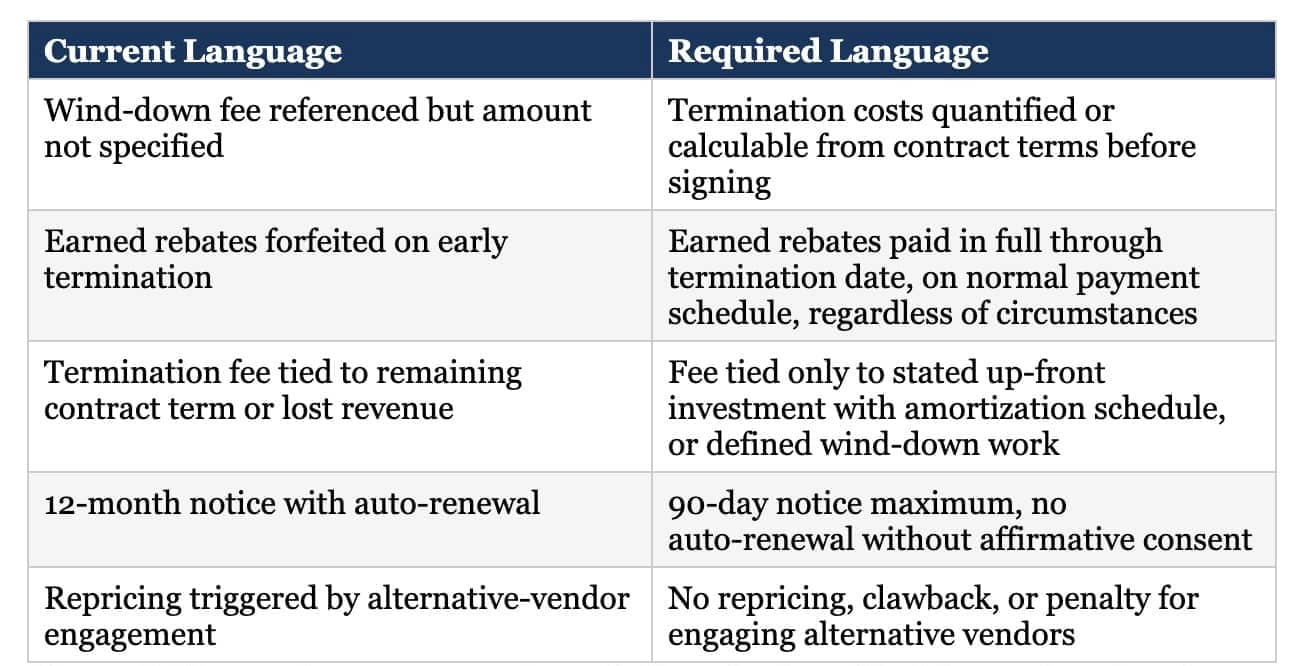

Undisclosed termination costs. The contract references a termination fee or wind-down cost without specifying the amount or method of calculation. The fiduciary cannot price the exit before signing. Fails Test 1.

Rebate forfeiture on exit. Earned rebates are forfeited if the plan terminates before the end of the plan year, before a specified rebate reconciliation window, or at all. The contract permits the PBM to retain plan assets the plan would otherwise be entitled to receive. Fails Test 2.

Lost-profits recovery. The termination fee is tied to remaining contract term, unearned future revenue, or damages disconnected from any cost the PBM actually incurred. The plan is paying for revenue the PBM did not yet earn. Fails Test 2.

Lock-in by notice. Notice requirements of twelve months or longer, sometimes combined with auto-renewal provisions that require affirmative action to exit. No fee is labeled. The notice period itself operates as the penalty. Fails Test 1.

Penalty structures triggered by alternative-vendor engagement. Repricing of remaining services, accelerated amounts owed, or credit clawback if the plan engages an alternative vendor before contract end. Fails Test 2.

A contract failing one pattern is a Red Flag. A contract stacking two or more is structurally locking you in.

What the Database Shows

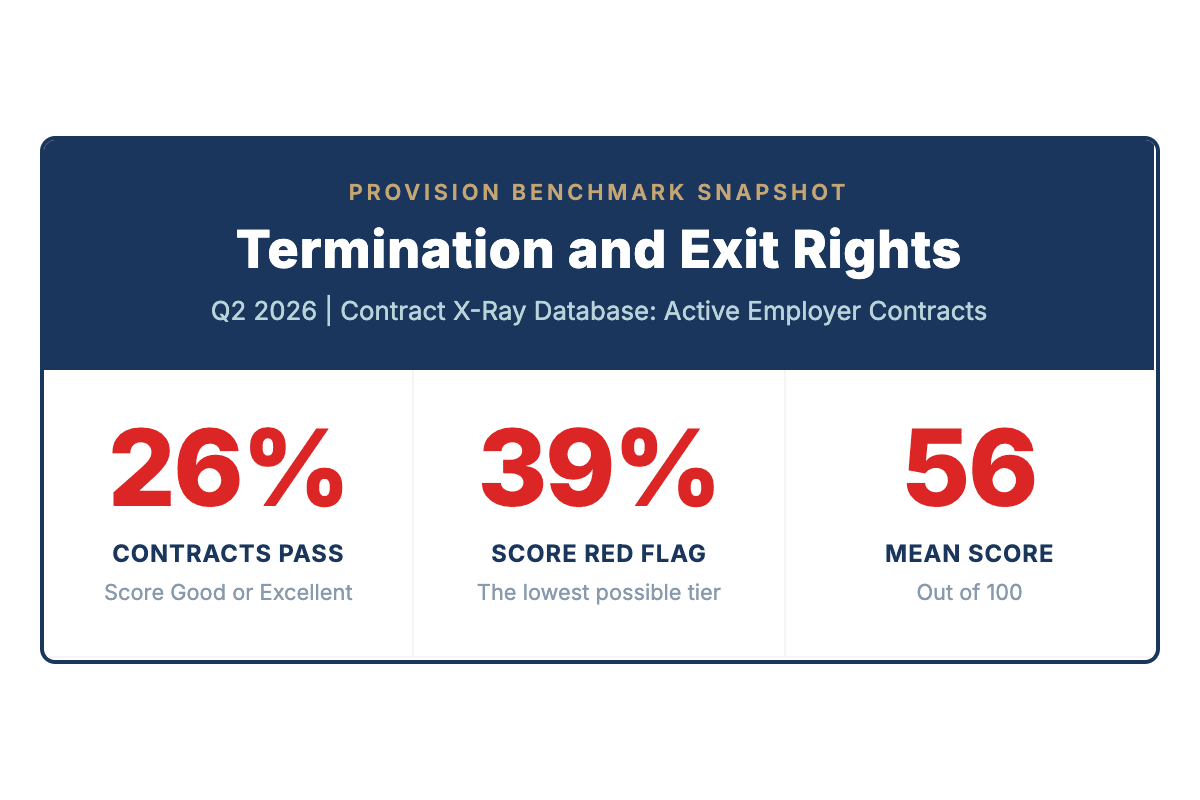

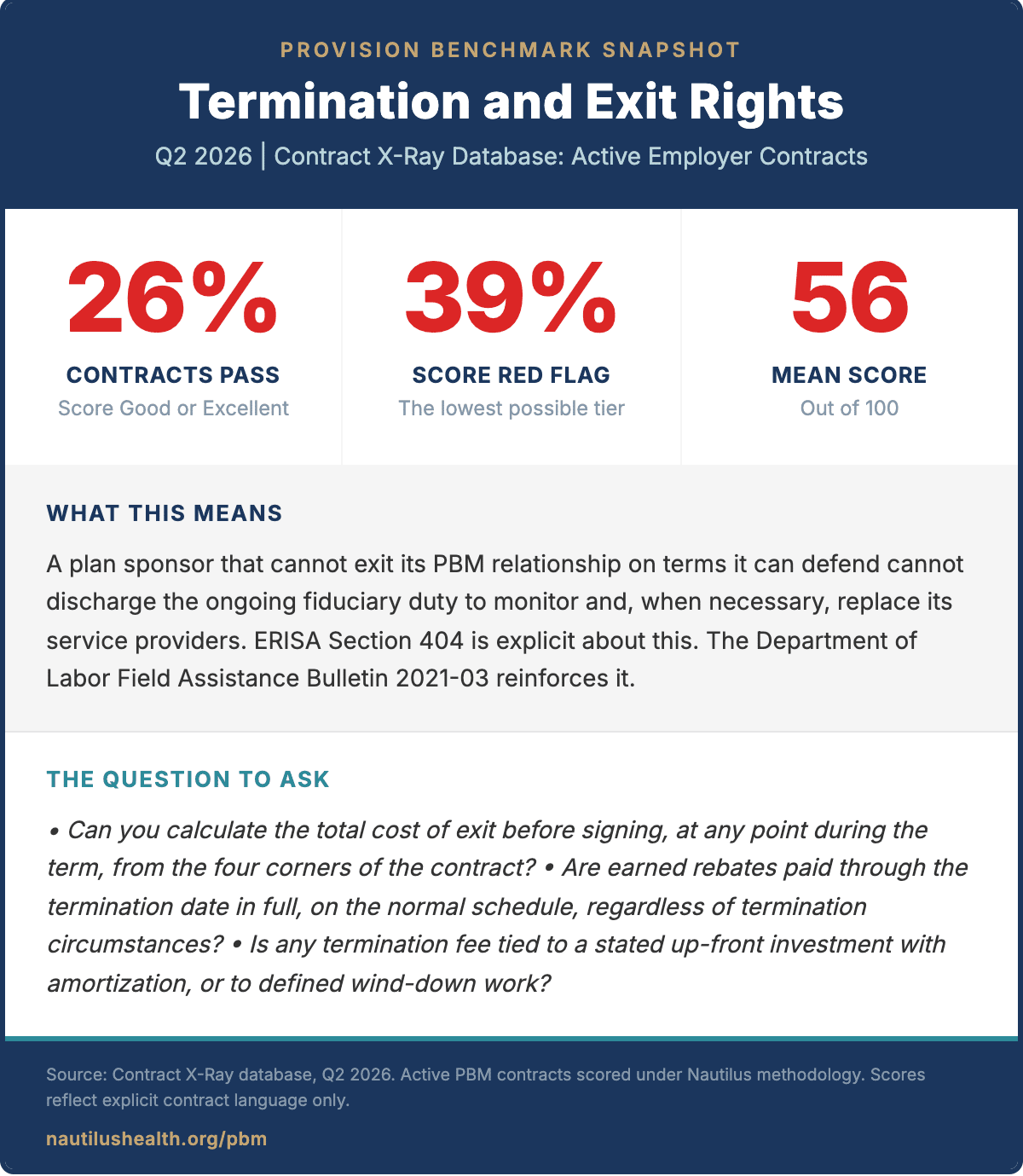

Termination and Exit Rights

Fifty-two percent of contracts sit below Fair. More than half fail one or both tests outright.

But notice the other end of the distribution. Twenty-six percent of contracts score Good or Excellent. The market has actually solved this provision. The fiduciary-aligned PBMs in the database meet both tests without difficulty. Some publish their termination terms openly. Some commit to no fee at all. The standard is achievable. The contracts that fail it fail by choice.

This is the difference between exit rights and other provisions we’ve benchmarked. Audit rights are uniformly bad across the market. Carve-out rights are uniformly bad across the market. Termination has a bimodal distribution. 26% of contracts pass cleanly. 39% fail outright. The middle is thin.

Your contract is likely on one side of the divide or the other. There is almost no third option.

Why This Matters

A plan sponsor that cannot exit its PBM relationship on terms it can defend cannot discharge the ongoing fiduciary duty to monitor and, when necessary, replace its service providers. ERISA Section 404 is explicit about this.

When the termination provision is structured so that the cost of leaving exceeds the cost of staying, the fiduciary obligation has been contractually nullified. The plan sponsor still owes the duty. The contract has just removed the practical ability to exercise it.

Three statutes converge on this single provision:

Section 403 governs the treatment of plan assets. Rebate forfeiture violates it.

Section 404 governs the ongoing duty of prudence. Lock-in violates it.

Section 408(b)(2) governs the reasonableness of service provider compensation. Disproportionate fees and lost-profits recovery violate it.

A contract that fails this Termination and Exit provision is not just a bad commercial deal. It is a contract that has impaired the fiduciary’s ability to do the job the law requires.

What Benchmark Data Changes

A single plan sponsor reading a single termination section sees boilerplate. The notice period looks standard. The rebate language looks technical. The wind-down fee looks routine.

With benchmark data, the conversation changes.

The active contracts in the database, the ones with 52% failing below Fair, represent what many employers signed in the past. But that’s not the whole picture.

Some PBMs are now offering “CAA 2026 Ready” contracts with exit provisions that score Excellent. These aren’t negotiated exceptions. They’re standard terms, offered to employers who know to ask for them.

You should expect the same from your PBM.

Language That Moves The Market

When your PBM says the termination language is standard, here’s how to respond:

Market Moving Language

If your PBM says these terms aren’t available, ask why 26% of the market already offers them.

What to Do First Thing Monday

Pull the termination section of your PBM contract and identify which failure patterns apply: undisclosed costs, rebate forfeiture, lost-profits recovery, lock-in by notice, or penalty on alternative engagement.

Answer three yes-or-no questions: Can you calculate the total cost of exit before signing, at any point during the term, from the four corners of the contract? Are earned rebates paid through the termination date in full, on the normal schedule, regardless of termination circumstances? Is any termination fee tied to a stated up-front investment with amortization, or to defined wind-down work?

Compare to the benchmark. If you cannot answer yes to all three, your contract fails the disclosed-and-reasonable standard. You’re in the 52% below Fair.

Submit your contract for scoring. Email support@nautilushealth.org. The benchmark grows one contract at a time and so does employer leverage.

In Closing

The cost of leaving should be a number you can write down, supported by something the PBM actually spent. If your contract makes it anything else, it’s not an exit provision. It’s a lock.

Fifty-two percent of contracts fail the disclosed-and-reasonable standard. But 26% pass cleanly.

The market has solved this. The question is which side of the divide your contract sits on and whether you’ll accept that when you sign your next one.

Here’s to clearer thinking, stronger plans, and better outcomes for the people who rely on us.

All the best,

P.S. Next week: Model language for audit, carve-out, and exit provisions. The provisions that make a contract CAA 2026 Ready.

Subscribe & Share

🔗 Subscribe: Was this newsletter forwarded to you? Signup to receive The Health Plan Compliance Advantage every Monday.

📤 Share: Know someone negotiating a PBM contract? Forward this issue. The three attorney questions alone could change the conversation.

💸 SPECIAL OFFER: Newsletter subscribers receive 10% off any Validation Institute service. Use code FIDUCIARY10 at checkout.

────────────────────────────────────────

Don’t be a bystander. Change the status quo and reap the benefits of The Health Plan Compliance Advantage. Schedule an introductory call with us.